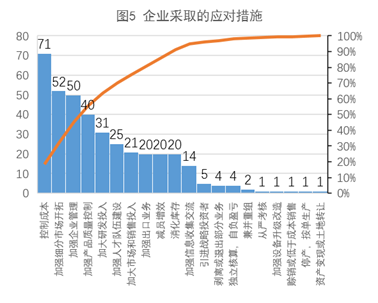

Abstract In 2015, the overall operation of China's machine tool industry continued to show a significant downward trend. Under the influence of domestic and international economic situation changes, traditional demand is sluggish, external competition is intensified, internal management difficulties and environmental uncertainties are intertwined, the machine tool industry is running...

In 2015, the overall operation of China's machine tool industry continued to show a significant downward trend. Under the influence of factors such as changes in the domestic and international economic situation, sluggish traditional demand, intensified external competition, internal operational difficulties and changes in environmental uncertainty, the operation of the machine tool industry has shown a state of inertia decline, and operational pressure has surged. Overall performance: traditional engine slowdown, industry downturn

According to a survey conducted by the China Machine Tool Industry Association on the 81 key enterprises in the industry, the industry boom index fell to 34.5% in 2015, down 8.8 percentage points from the same period in 2014, and the industry was in a downturn.

Subdivision: Operation evolves from differentiation to assimilation, and structural contradictions are prominent

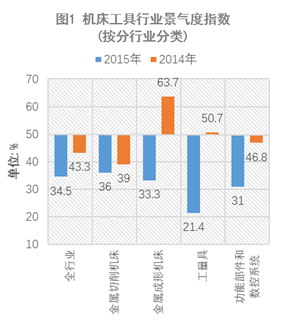

From the perspective of different sub-sectors and ownership enterprises, the 2015 prosperity index is far below the 50% equilibrium line, and it shows a different degree of decline compared with the same period in 2014. Therefore, the industry climate index reflects that the industry operation in 2015 has begun to evolve from the operational differentiation before 2014 to the assimilation of the downturn.

Judging from the changes in the prosperity index of different sub-sectors, the industrial equipment and metal forming machine tools that were more stable before 2014 showed a sharp decline, ranking first in the ranking of the prosperity index from low to high (21.4). %) and third place (33.3%), while metal cutting machines that had previously continued to drop significantly were ranked fourth (36%). This new change can be seen more clearly from the decline in the boom index. The descending order is from metal forming machine (30.4%), measuring tool (29.3%), functional components and CNC system (15.8). Percentage), metal cutting machine tools (3 percentage points). Based on the above two aspects and actual operation, the following characteristics can be summarized:

â— The adverse impact of structural contradiction between supply and demand on the machine tool industry is spreading from the local to the whole industry. Due to the different composition, market structure, management factors and environmental factors of different sub-sectors, the speed of diffusion is affected, and then the early stage is presented. Run the process of differentiation that differentiates into the current convergence.

â— From the actual operation of the metal forming machine tools, measuring tools, functional components and numerical control systems, which have experienced a sharp decline in the prosperity index, the market demand for low-end products has shrunk sharply, which is the main external cause of its downturn, and related sub-sectors. The low proportion of the low-end product structure and the lack of transformation and upgrading are the main internal factors of its downturn.

â—Since the metal cutting machine tool industry has been suffering from the market impact caused by the structural contradiction between supply and demand since 2011, the low-end production capacity has been relatively shrinking. As a result, the 2015 boom index showed only a slight decline. However, due to the prominent structural contradiction between supply and demand, it is still in the operation of the metal cutting machine tool industry. In 2015, its prosperity has been greatly reduced.

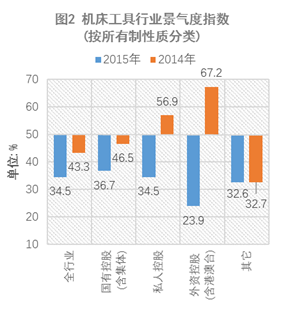

It can also be seen from the changes in the business climate index of different ownership systems that there are signs of a downturn in the industry. In 2014, the foreign-funded holdings (including Hong Kong, Macao and Taiwan) and privately-held corporate climate index also showed significant expansion trends, which were 67.2% and 56.9% respectively. In 2015, foreign-controlled enterprises (including Hong Kong, Macao and Taiwan) and privately-held enterprises had a large business climate index. The decline showed significant shrinkage, at 23.9% and 34.5%, respectively, with a decrease of 43.3 and 22.4 percentage points respectively. The above changes are very evident in companies with different ownership characteristics. As foreign-invested holdings (including Hong Kong, Macao and Taiwan) and privately-held companies have always been the most flexible internal mechanism, responding to the market changes the fastest, and also the industry group with the least impact in the down-front period, the significant contraction of the prosperity index confirms that the downturn is in the industry. The judgment of proliferation.

Prominent problems: internal and external factors lead to weakening of the development of the industry, "training internal strength" is still the key

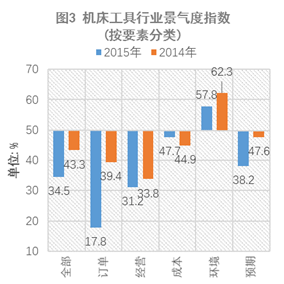

From the various operational factors and expected prosperity index, the driving force of the industry's development has seriously declined, which in turn affects the confidence of the industry. Among the operational factors such as orders, operations, costs and environment, the contract contraction was the most serious, only 17.8%, down 21.6 percentage points compared with the same period in 2014; the business contraction degree followed the order in the second place, 31.2%. Compared with the same period in 2014, it decreased by 2.6 percentage points.

Orders and operating factors reflecting operational dynamics and quality in the operational factors showed a significant contraction, which echoed the industry's development expectations and also showed a significant contraction of 38.2%, down 9.4 percentage points from the same period in 2014.

[Introduction to the background of the machine tool industry boom index]

â— The index is an annual questionnaire survey conducted by the China Machine Tool Industry Association for key industry contacts in December. The annual industry sentiment index is calculated based on the returned questionnaire.

â— The index is a comprehensive index consisting of orders, operations, costs, environment, and expected five categories of individual indicators. The weights of each individual indicator are 30%, 20%, 20%, 10%, and 20%, respectively. The cost is reversed to make it consistent with other metrics. The diffusion index can be an overview of the overall trend. The index is greater than 50%, indicating that the economy is rising, the industry is expanding or prosperous; the index is less than 50%, indicating that the economy is declining and the industry is in a state of recession or depression. (Du Zhiqiang, Information and Statistics Department, China Machine Tool Industry Association)

Metal Polishing Wax Paste Compounds

Metal Polishing Wax Paste Compounds,Blue Polishing Wax,White Polishing Paste Bar,Car Polishing Liquid,compound bar

NINGBO HENGHUA METAL SURFACE TREATMENT TECHNOLOGY CO.,LTD. , https://www.henghuametal.com